RESEARCH & INSIGHTS

ACA Subsidy Expiration: What Behavioral Health Practices Need to Know Now

Survey findings and practical guidance for navigating the coverage disruption

Celeriti Practice Management | Ethan Sena | March 2026

Key Takeaways

- ACA enhanced subsidies expired December 31, 2025. Premiums roughly doubled, and 4–5 million Americans are expected to drop coverage.

- In a survey of 80 behavioral health practices, 80% say their top concern is patients dropping out of care entirely — and one-third have already seen patients discontinue treatment.

- Practices should act now: verify coverage status, prepare for cost conversations, and reach out to at-risk patients before they disappear.

- Legislative relief is possible — the House passed an extension — but timing remains uncertain. The impact of the coverage gap will be felt regardless of what happens in Washington.

The expiration of ACA enhanced subsidies is already affecting behavioral health practices across the country. Based on a survey of 80 practices conducted in February 2026, this article examines the impact providers are seeing, their top concerns, and practical steps practices can take to prepare.

In January of this year, KFF Health News spoke to Robert and Emily Sory, a couple who run an animal rescue in Nashville, Tennessee. In 2025, they purchased insurance through the Affordable Care Act. When premiums on their plan roughly doubled for 2026, they made a difficult decision: go without coverage entirely.

They are not alone. Across the country, millions of Americans are facing the same calculus – and behavioral health practices are watching their patients make similar choices in real time.

What Happened

In March 2021, Congress passed the American Rescue Plan Act, which included enhanced subsidies that significantly increased federal assistance for Americans purchasing coverage through ACA marketplaces. The subsidies worked: ACA enrollment grew 88%, from 11.4 million in 2020 to 21.4 million by 2025 (KFF.org).

Those subsidies expired on December 31, 2025. Congress was unable to extend them, with a vote falling short at 51–48. The result: premiums roughly doubled for more than 20 million subsidized enrollees. KFF projects an average premium increase of 114% for 2026. The Urban Institute and Commonwealth Fund estimate that 4.8 million Americans will drop coverage this year, with younger and healthier enrollees most likely to leave the market first.

How This Affects Behavioral Health Practices

For behavioral health practices, the subsidy expiration creates a cascade of challenges that compound over time.

The Immediate Shock

Patients face dramatically higher premiums and must decide quickly whether to pay, downgrade to a high-deductible plan, or drop coverage entirely. Many are making these decisions without fully understanding the implications for their care.

The Rationing Effect

Patients who stay covered but switch to high-deductible plans suddenly have significant out-of-pocket costs for every session. The predictable response: they start spacing out appointments, skipping sessions, or asking to reduce frequency. For behavioral health, where continuity of care is clinically essential, this rationing is particularly damaging. Treatment gaps can lead to relapse, crisis, and worse outcomes.

The Dropout Risk

Some patients will leave care altogether — not because they want to, but because they cannot afford it. Unlike a deferred medical procedure, discontinued therapy often means losing the therapeutic relationship and starting over if they return.

The Compounding Effect

Adding to the pressure, major insurers like Aetna/CVS have exited ACA markets in multiple states, leaving patients with fewer options and forcing plan changes that disrupt established provider relationships.

For practices, these forces converge into volume declines, rising bad debt, and cash flow pressure — all while managing the clinical complexity of patients under financial stress.

What We Found

To understand how practices are experiencing these changes, we surveyed 80 behavioral health practices in February 2026. The results confirm that the impact is real, immediate, and concerning.

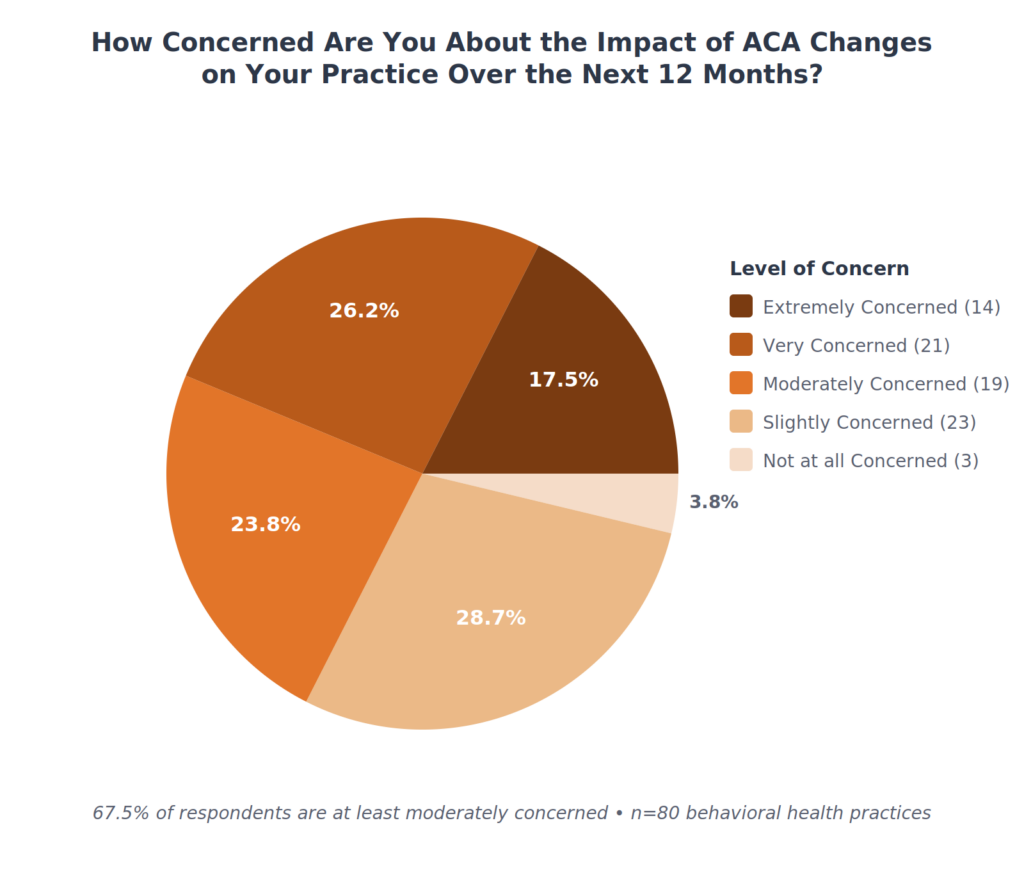

Practices are worried. When asked about their level of concern regarding ACA changes, 67.5% of respondents reported being at least moderately concerned, with 43.8% saying they are very or extremely concerned. Only 3.75% said they are not concerned at all.

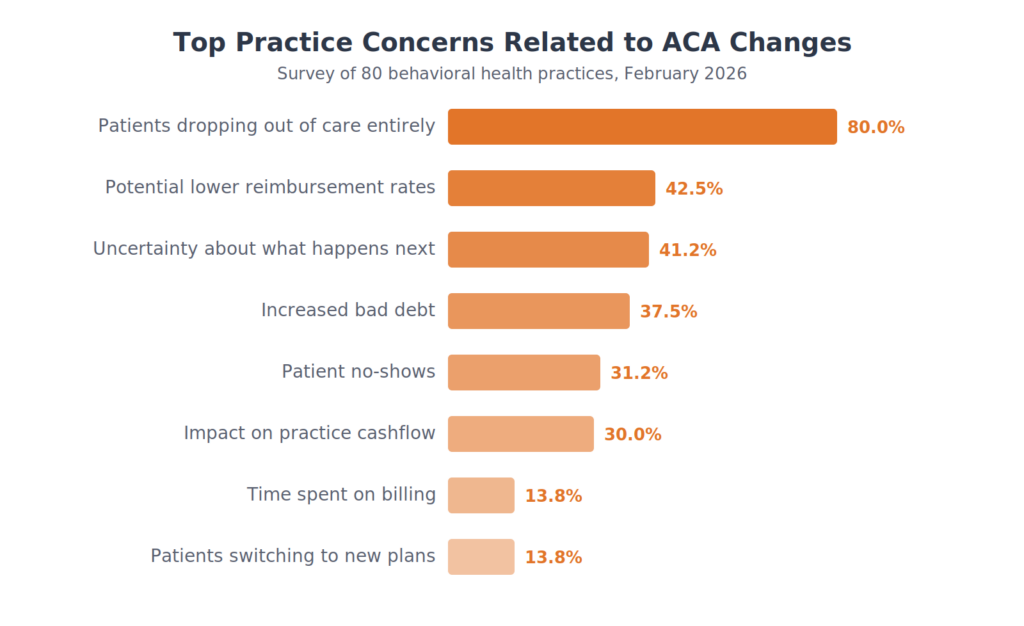

The top concern is clear: 80% of respondents say their biggest worry is patients dropping out of care entirely. This outranks concerns about bad debt (37.5%), cash flow (30%), and reimbursement rates (42.5%). Behavioral health providers understand what research confirms: when patients leave treatment, outcomes suffer.

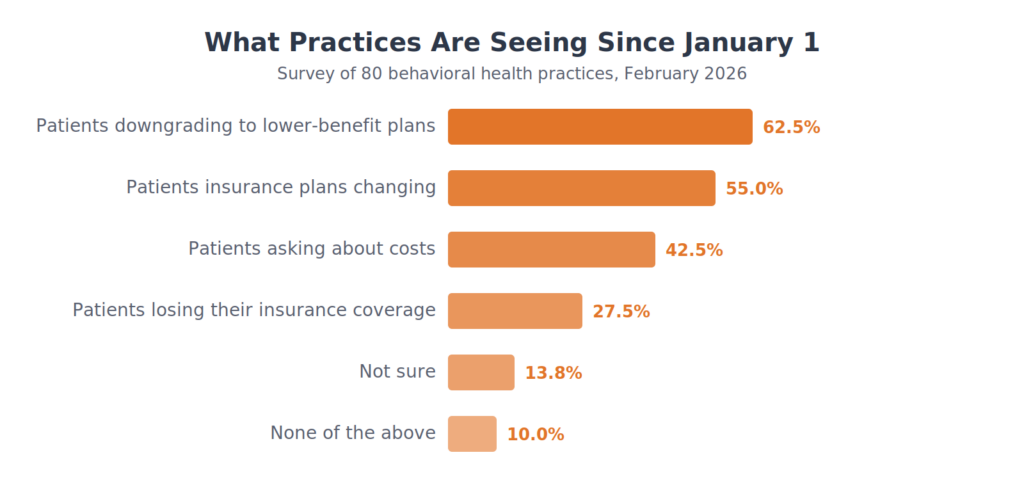

It is already happening. When asked what changes they have observed since January 1:

- 62.5% report patients downgrading to higher-deductible or lower-benefit plans

- 56% report patients asking to reduce visit frequency

- 33.8% have already seen patients discontinue treatment entirely

- 27.5% have been directly affected by insurers leaving the ACA market

These are not projections. They reflect what practices are experiencing right now, barely six weeks after subsidies expired.

“I’m concerned about the feasibility of my practice and individual psychotherapy as a whole if insurance plans become unaffordable or have extremely high deductibles. The only way this works is if therapy is subsidized via affordable health care.”

— Survey Respondent

“Since many therapists rely on the ACA for their own coverage, it makes it that much more difficult to take care of themselves so that they can be healthy and in the mindset to support their clients.”

— Survey Respondent

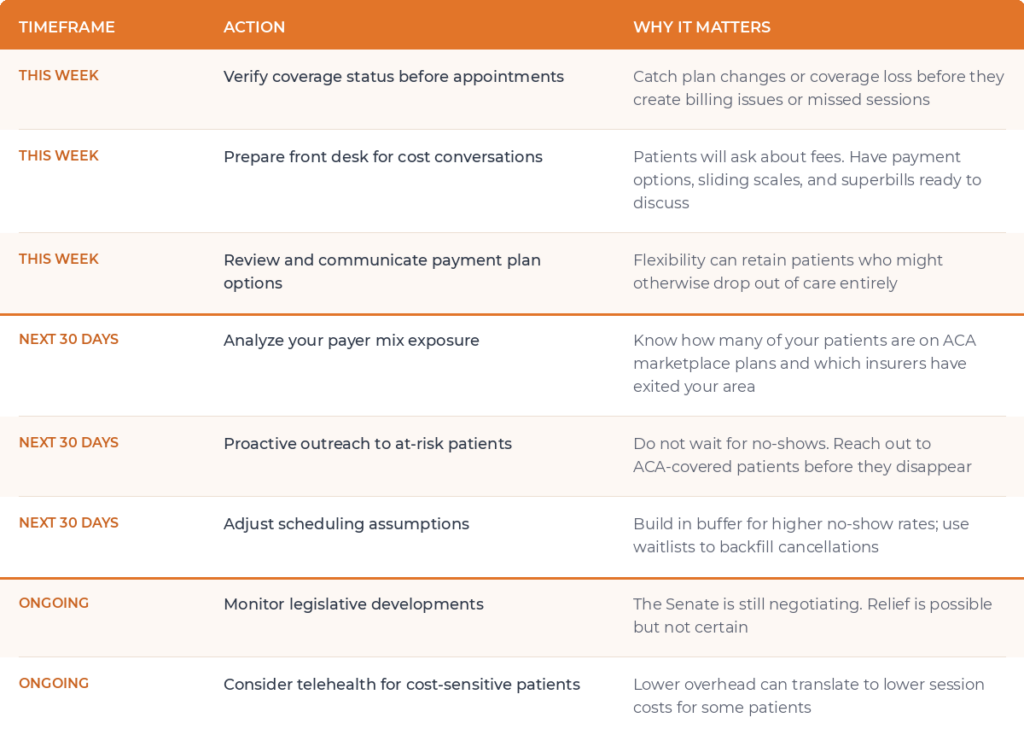

What Practices Should Do

While the policy landscape remains uncertain, practices can take concrete steps now to support their patients and protect their operations.

What Comes Next

There is reason for cautious optimism. In January, the House of Representatives passed a three-year extension of ACA enhanced subsidies. However, the Senate has not scheduled a vote, and the outcome and timing remain uncertain.

Even if subsidies are eventually restored, the coverage gap that began in January 2026 will have lasting effects. Some patients who dropped coverage or discontinued treatment will not return. Others who are “toughing it out” now may reconsider as months pass and costs accumulate. Practices should prepare for the possibility that the worst is still ahead.

Resources

This article is based on a survey of 80 behavioral health practices conducted February 2–13, 2026, by Celeriti Practice Management. For methodology and full results, contact Celeriti.